If you are an opportune customer to join one of the leagues of e-whatever, you will use electronic payments (e-payment) as an instrument to pay your bills. As you might argue, by using this gizmo, you’ll avoid yourself from hectic queues in cashing your money at the bank. Subsequently, you can pay your bills without using cash taken from your pocket. E-payment also eases us to make various transactions at a single point with the facility of one stop payment service. With an ATM on hand, you can now pay bills of your telephone, mobile phone, electricity, internet, insurance, credit card and so on. Now, thanks to innovation, e-payment has been diversified to a different mode of payment known as the e-wallet.

The latter is quite interesting. Although people have been familiar with debit cards for quite some time, the inception of e-wallet as a method of electronic payment is quite recent in Indonesia. In the country, e-wallet was introduced by two issuers, bank Mandiri and Telkomsel. E-wallet issued by the former has the anatomy similar to those in credit or debit cards. A certain amount of money must be filled before used for transactions. Consumers can fill their e-wallet at the ATM machine. During a transaction, the cashier swipes the card and puts the transaction value. The value deducted from the e-wallet wraps up the transaction.

On the other hand, the T-Cash of Telkomsel employs the user’s mobile phone as a medium to perform transactions. The SIM card inside the phone functions both as the mobile signal activation and as the wallet. The user fills the e-wallet at the ATM. Transaction is carried out by notifying the user’s phone number. The cashier will type in the phone number on the cashier machine. The amount of money in the wallet will appear on the screen. The cashier then deducts the wallet based on the transaction value charged to the customer.

Transaction cost strategy

Through the lens of strategic management, the use of e-wallet reduces transaction costs and shortens transaction time. Customers do not spend their time to cash in their money since they can use their e-wallet to pay their bills. From the merchant perspective, the adoption of the e-wallet cuts transaction time as well. Furthermore, with the pervasive use of e-wallets, merchants can start eliminating changes on the cashier machine. Payment verification activities such as those exhibited in credit or debit card transactions can be shortened since the e-wallet contains the money. This is quite different with a credit card payment in which a clearinghouse must verify both the merchant identification and the credit card status before the transaction proceeds. The e-wallet transaction is also faster than the debit card since the only thing required, except for some security reasons, is the amount of money contained in the wallet.

But the question remaining is in what way the use of e-wallet will pay off. How does it differentiate with credit and debit cards? What’s the real advantage of using e-wallet? Put it simply, will e-wallet work in Indonesia?

To answer the question, I will first assess two fundamental factors in analyzing the transaction cost strategy: the system and the market. I will address some system issues attributed to e-wallet issuers if they want to commercialize this payment method. Then, I will scrutinize the market of e-wallet. Specifically, the essay will assess the segmentation of the e-wallet through the lens of the customer attitude. From these factors, I will advise the future of e-wallet in Indonesia and provide some recommendations for e-wallet issuers to diffuse this payment method.

The system

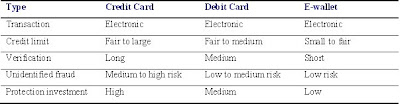

It can be noticed that the concepts of e-wallet is derived from those in credit and debit cards. The real difference lies on the credit limit assigned to the e-wallet (both on SIM or “ordinary” card) and the refilling system. As it serves as a wallet, e-wallet issuers assign lower credit limits to the e-wallet than those given to credit and debit cards. Consequently, the security attached to the e-wallet system is rather loose compared to its two counterparts. Once the amount of money in the wallet is not sufficient, the user should know from the merchant that the transaction cannot be completed. Moreover, since the credit limit is relatively low, frauds can be identified earlier (e.g. during transactions) than those in debit or credit cards (Table 1). E-wallet users can detect irregularities once they use their wallet on the cashier machine. Lower limits assigned to the e-wallet and the refilling method eases the e-wallet holder to identify suspicious and unknown transactions. The refilling method forces the holder to fill the e-wallet, thus avoiding further money losses to the authentic owner.

Table 1. Comparison between credit card, debit card and e-wallet

Based on characteristics given in Table 1, we can draw some insights on benefits of the e-wallet as described in Box 1.

Box 1. Benefits on using e-wallet

From benefits given in Box 1, it appears that the use of e-wallet has better offers than the use of credit and debit cards. However, we need to see the market assessment, specifically on the market segmentation before drawing conclusions and suggesting recommendations on the use of the e-wallet.

The market

Based on the system characteristics discussed above, it can be suggested that the use of e-wallet is a better proposition than debit or credit cards. From the customer perspective, e-wallet is a manageable electronic payment. The refilling system attached to the e-wallet enables users to control their spending, thus avoiding excessive money usages. If it is so, then we could promulgate that the use of e-wallet should cover larger market demographics to gain the economies of scale. Therefore, we could expect e-wallet adoptions not only confined in large cities but also in small/mid towns and even municipals.

However, I believe the pervasiveness of e-wallet will pose challenges if we assess the market of electronic payments. Although the e-wallet is a promising payment method once it reaches the economies of scale, permeating this payment for larger demographics requires infrastructures supporting e-payment systems. This means that the targeted region must have been connected with e-wallet systems both on the issuers and the merchants.

While most of the large cities in the nation have been equipped with such infrastructures, similar networks may not be available in mid/small cities/towns. Even if they exist, such infrastructures (e.g. ATMs and e-payment devices) may not be equally distributed throughout the targeted region. One cannot even expect the availability of these networks in municipals. Thus, the adoption of e-wallet is hampered by the lack of system availabilities easing customers in using their e-wallets.

Box 2. Challenges on the implementation of e-wallet

Second, people living in mid/small cities/towns may not be used to electronic payments. Conservative payments may dominate the region. A limited number of electronic payments may exist in mid/small cities but the percentage of users using such payments will not be significant in commercializing the use of e-wallet. As a result, the adoption of the e-wallet will have difficulties in reaching the economies of scale.

We can presume that the adoption of e-wallet can only be acceptable in large cities. However, I believe that e-wallet issuers do not elevate the segmentation and differentiation of the e-wallet. Until now, the attitude of using e-wallet is indifference. People do not perceive the advantage of using this payment method compared to credit and debit cards. E-wallet is considered as a payment method overlapped with credit or debit cards. They may not even know that such product exist. I do not see campaigns to promote e-wallet in public spots especially in shopping centres where credit card issuers frequently set up stands to attract customers. Nor do I see advertisings on newspaper to penetrate this payment method.

Therefore, it appears that the e-wallet may lose its market shares over credit and debit cards should the issuers do not come up with a solid proposition distinguishing the use of e-wallet and its counterparts.

Conclusion

E-wallet is a new method to fill the “reach” gap on transaction payments. Either through the plastic or SIM card type, people assume that e-wallet is a substitute of both credit and debit cards. However, looking at the credit limit assigned to e-wallet, there is a misconception on when and where to use the e-wallet.

Challenges in commercializing the e-wallet are due to the limited users. E-wallet is expected to be used not only in large cities but also in small and medium cities. Yet, the network supporting the system may have not been equally distributed or even unavailable; leaving the pervasiveness of the e-wallet confined to the area where the infrastructures are clustered.

The adoption of the e-wallet poses challenges as it competes with debit and credit cards. People may be confused on when and where they use their e-wallet. Merchants may become dubious due to the limited consumers using this method. Thus, the hesitant use of the e-wallet creates multiplier effects hampering the pervasiveness of this payment method.

Recommendation

We expect e-wallet issuers invest in marketing activities making the e-wallet more appealing for customers. However, some crucial highlights that can be suggested for e-wallet issuers are related to the networking system supporting the e-wallet and the market differentiation of the e-wallet relative to its substitutes (Box 3).

Issuers should not attempt to enter e-wallet markets unless they ensure the availability of infrastructure supports. This is not only restricted to the infrastructure but also the consumer attitude within the targeted demographics. Since prerequisites to induce the customer are the availability of the networking system and the adoption of the e-payment by merchants, e-wallet issuers should invest on infrastructures and distribution (e.g. merchant) channels, either through self investing or through cooperation with financial institutions.

Box 3. Recommendations for e-wallet issuers to permeate e-wallet

The pervasive diffusion of the e-wallet is also related to e-wallet acceptances by credit and debit card users. Since these users may have decided occasions in using their cards, e-wallet issuers must define, identify and develop differentiation strategies to place e-wallet at different markets. I believe that cooperating with small and mid size merchants is a niche for e-wallet issuers in dispersing this payment method. E-wallet should be positioned as a payment method replacing a wallet. Thus, e-wallet markets should not intersect too much with debit and even credit card markets.

{kind=link}